50% Chinese shipping business - bulk carriers, in Africa: vessels

For Bloggers

A challenge to manage China to Africa Shipping Business?

Contact us here mayado@sylodium.com

Make money with us

For companies

Make business in all bilateral trades, shipping business from China to Africa

For Institutions

Tap Sylodium for synergies to conquer Chinese - African trade relations in Internet

This new is from ThisDayLive.com

The Place of Developing Countries in Global Maritime Business

Eromosele Abiodun examines the United Nations’ Conference on Trade and Development Review of Maritime Transport, submitting that the long-term growth prospects for seaborne trade and maritime businesses are positive

Before now, the global maritime business was dominated by Western countries. That appears to be changing as it has emerged that developing countries are increasing their involvement in many parts of global maritime business. Aside expert’s position on the development, the review of maritime transport 2016, published by the United Nations Conference on Trade and Development (UNCTAD), this month, laid credence to this.

The review however, outlined a cautiously upbeat view of global shipping over the years ahead. This is correct because just before the election of Donald Trump as president of the United States. Following his rhetorics during his campaign, the risks for world trade appear to have suddenly multiplied or, at least, uncertainty has been abruptly amplified by this election outcome. Trump had criticised globalisation and free trade, expressed hostility towards international trade pacts and shown enthusiasm for a protectionist stance. What is not clear yet is how much was campaign rhetoric and how much was firm intention. If government policy evolves on this basis, a potentially highly unstable period for world trade could result, where detrimental influences are a bigger feature. However, that is speculation and may remain so until the Trump administration outlines its plans. However, the report suggests that long-term growth prospects for seaborne trade and maritime businesses are positive, although there are many uncertainties and downside risks. Analysis of the report points to ample opportunities for developing countries to generate income and employment and help promote foreign trade.

Ship Supply Questions

Meanwhile, an analysis of the entire world fleet of commercial vessels by country of ownership revealed that three countries remained at the top. Greece was still by far the largest owning country with 293 million deadweight tonnes, 16.4 per cent of the 1792 million dead weight tonnes world total. Japan was the second largest, with 229 million dead weight tonnes (12.8 per cent) and China was in number three position with 159m dwt (8.9 per cent). Accompanied by Germany (119 million dwt) and Singapore (95m dwt), the top five owning countries comprised exactly half of the world total.

The UNCTAD report discussed the structure, ownership and registration of the world fleet of ships. It pointed out that the fleet’s deadweight capacity (all ship types) grew by 3.5 per cent in 2015. While this increase was the lowest annual percentage for over a decade, it was still far higher than the 2.1 percent growth in demand, resulting in continued global overcapacity.

The authors focussed on various positive indicators for shipping markets. However, there was discussion about the downside of the huge container ships surplus caused by overinvestment, which the review suggested was not in the long-term interest of either liner operators or shippers. In the short term shippers may benefit from lower container freight rates but, in the long term there is a danger of more markets with oligopolistic market structures, reflecting a continued process of concentration as service operators become fewer.

Ship Demand Conundrum

Experts believe UNCTAD’s view of the seaborne trade outlook seems realistic at present and, to some extent, provides a counterpoint to alternative more pessimistic projections emerging during the past twelve months or so. But the report conceded that negative developments in the macroeconomic framework are intensifying, and dampening maritime cargo volumes. Nevertheless, the experts argued that growth in global seaborne trade is still intact. “While China’s slowdown is bad news for shipping, a number of developing countries are becoming more involved and could drive further trade enlargement, “said the National President of the National Council of Managing Directors of Licensed Customs Agents (NCMDLCA), Lucky Amiwero.

Uncertainties and downside risks listed in the report included: weak global demand and investment, political uncertainties such as the ongoing migration crisis, doubts about the future pace and direction of European integration and a further loss of momentum in developing countries. Moreover, another set of factors were identified – technology, innovation, the data revolution and e-commerce – which can transform and disrupt the shipping industry, generating both challenges and opportunities. How will these trends evolve? The report admitted the outcome was unknown.

Among causes for anxiety about the future evolution of world seaborne trade was prominent, along with the shared and circular economies. However, the report did not comment specifically on the likely timing of most of the impact from these trends. What seems clear though is that these are longer-term influences evolving over a decade or two perhaps and, as a result, immediate effects may be limited. Reduced global use of fossil fuels is another, more tangible, worry for the shipping industry because it is already highly visible.

The fourth industrial revolution is a concept which envisages that innovation, technology and big data could assist in increasing efficiency and productivity in the global economy. This progress, experts believe, could shift established modes of production and consumption, with negative implications for seaborne trade.

Experts also believe that the performance of supply-chains could be enhanced, accompanied by a reduction in their typical length as features such as three-dimensional (3D, or additive) printing and robotics are increasingly incorporated.

Shorter supply-chains, they added, implied shorter average sea voyage distances, with adverse effects on the demand for shipping services.

“Similarly, the impact of the shared and circular economies points to savings and efficiency gains which could lower demand for maritime transport. Shared economy characteristics (renting and swapping, for example) may modify demand and also supply chains. This would be achieved through new technology and platforms that facilitate asset management, service delivery and information access.

A circular economy promotes effective use of resources, greater resource conservation, and reduced reliance on fossil fuels and raw materials, to achieve sustainable production and consumption patterns. Steps have been taken already in numerous countries to cut fossil fuel consumption. Further advances in renewable energy production and energy storage could have a large adverse impact on oil, coal and liquefied gas movements and associated demand for shipping capacity, “Amiwero submitted.

Developing Countries’ Maritime Strengths

Many developing countries are involved in five key aspects of the global shipping scene – ship owning, ship registration, seafarer supply, shipbuilding and ship recycling. As the UNCTAD report emphasised, in some activities developing countries are top participants, with increasing shares of the world market. The report suggested that a good policy choice for policymakers in these countries is to identify and provide support for selected maritime businesses in sectors where a comparative advantage is evident.

According to the report, for developing countries as a group (including transition economies) their ownership share of the global fleet total, as at the beginning of 2016, was just over two-fifths (40.5 per cent) and has been rising. Most of this capacity is owned in Asia, and just over half of that Asian sub-group is comprised of three countries/territories, China, Singapore and Hong Kong (China), jointly owning 19.1 percent of the world fleet’s deadweight tonnage.

A breakdown of the fleet owned in Asian developing countries, by ship type, shows that almost half consists of bulk carriers, one quarter is comprised of tankers, and one eighth is container ships. For comparison, in other developing country regions with much smaller tonnages, the breakdown is very different. Fleets in developing countries in Africa and the Americas have high shares of offshore supply vessel ownership, for example.

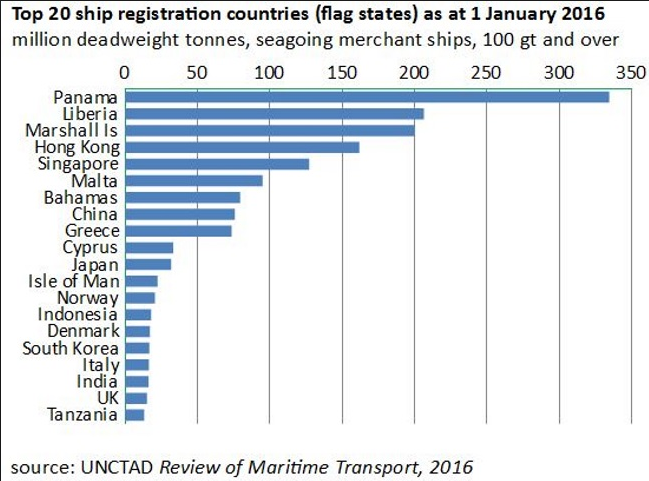

As is well known, ship registration in the global fleet is highly concentrated in developing countries. The report showed that, as calculated at the beginning of 2016, this group registers just over three-quarters (76 percent) of the world fleet’s deadweight tonnage. The top 5 flag states are all in this category, jointly registering 57 per cent of the world total. Panama is the largest, with 19 per cent, followed by Liberia (11 per cent), Marshall Islands (11 per cent), Hong Kong, China (9 percent) and Singapore (7 percent). Providing seafarers for the international shipping market is another large and strongly evolving activity for developing countries.

“Figures for 2015 were drawn from a survey conducted jointly by BIMCO and the International Chamber of Shipping, published several months ago. These show China contributing the largest number at 244,000 (15 percent of the world total). In second place was Philippines with 216,000 (13 percent), followed by Indonesia’s 144,000 (9 percent). Russia, India and Ukraine also provided substantial numbers. Global demand for seafarers apparently increased by a cumulative 45 percent during the decade ending last year, facilitating the expanding involvement of developing countries, “UNCTAD said.

A positive perspective

The report highlighted the lacklustre growth of global seaborne trade, currently increasing at a pace notably slower than the historical average, and the slowest since the debilitating world economic recession seven years ago. It also revealed uncertain prospects in the immediate future and further ahead, emphasising prominent downside risks.

Surplus capacity, it revealed, is compounding the problem for the shipping industry, with fleet expansion still exceeding demand enlargement across the shipping market as a whole.

The report revealed that there are ample opportunities for developing countries to generate income and employment and help promote foreign trade. A breakdown of the report showed that shipments expanded by 2.1 per cent, a pace notably slower than the historical average. The tanker trade segment recorded its best performance since 2008, while growth in the dry cargo sector, including bulk commodities and containerised trade in commodities, fell short of expectations. While a slowdown in China is bad news for shipping, other countries have the potential to drive further growth. South-South trade is gaining momentum, and planned initiatives such as the One Belt, One Road Initiative and the Partnership for Quality Infrastructure, as well as the expanded Panama Canal and Suez Canal, all have the potential to affect seaborne trade, reshape world shipping networks and generate business opportunities. In parallel, trends such as the fourth industrial revolution, big data and electronic commerce are unfolding, and entail both challenges and opportunities for countries and maritime transport.

Maritime Businesses

The report showed that the world fleet grew by 3.5 per cent in the 12 months to 1 January 2016 (in terms of dead-weight tons (dwt)). This, stakeholders said, is the lowest growth rate since 2003, yet still higher than the 2.1 per cent growth in demand, leading to a continued situation of global overcapacity. Different countries, it added, participate in different sectors of the shipping business, seizing opportunities to generate income and employment.

“As at January 2016, the top five ship owning economies (in terms of dwt) were Greece, Japan, China, Germany and Singapore, while the top five economies by flag of registration were Panama, Liberia, the Marshall Islands, Hong Kong (China) and Singapore. The largest shipbuilding countries are China, Japan and the Republic of Korea, accounting for 91.4 per cent of gross tonnage constructed in 2015. Most demolitions take place in Asia; four countries – Bangladesh, India, Pakistan and China – accounted for 95 per cent of ship scrapping gross tonnage in 2015. The largest suppliers of seafarers are China, Indonesia and the Philippines, “it stated.